June 2026 | Property

“The single biggest problem in communication is the illusion that it has taken place.” (George Bernard Shaw)

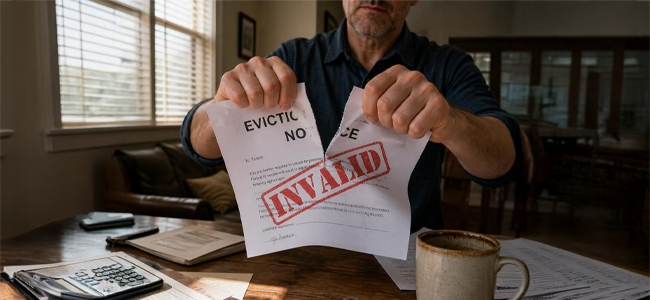

Many landlords assume that once a tenant stops paying rent, an eviction order will inevitably follow. A recent Western Cape High Court judgment shows how wrong that assumption can be. Despite rental arrears of more than R46,000 and an apparently legitimate grievance, a landlord’s eviction application failed because of a problem many people overlook: the cancellation letter.

The dispute arose after tenants allegedly fell behind on their rental payments. The landlord sought to terminate the lease and evict the occupants. Although the alleged arrears were not seriously disputed, the case ultimately turned on a different question: whether the lease had been validly terminated in the first place.

The court didn’t even consider whether the eviction itself would have been justified. Instead, the application failed because of defects in the cancellation process.

Why the cancellation failed

The letter sent to the tenants purported to cancel the lease immediately because of the rental arrears. At the same time, it gave the tenants a future date by which they had to vacate the property and demanded payment of the outstanding amounts.

The difficulty was that the letter appeared to communicate several different and potentially contradictory things at once. Had the lease already been cancelled? Were the tenants being given an opportunity to remedy the breach? Would payment of the arrears change anything? The notice did not provide clear answers.

The court confirmed an important principle of South African law: a notice terminating a lease must be clear, unconditional and unequivocal. If a notice leaves uncertainty about the parties’ rights and obligations, it may be invalid.

In this case, the court found that the cancellation notice was ambiguous. Because the lease had not been validly terminated, the landlord could not establish that the occupants were unlawfully occupying the property. Without unlawful occupation, the eviction application could not succeed.

A costly lesson for landlords

For landlords, the lesson is straightforward. Even where a tenant owes substantial rental arrears, a defective cancellation process can derail an otherwise strong case. Before launching eviction proceedings, it is essential to ensure that all notices have been properly drafted and served, and that all requirements for a valid termination have been satisfied.

For tenants, the case demonstrates that the outcome of an eviction application is not determined solely by whether rent is owing. A landlord must also show that the lease was lawfully terminated before a court will consider whether an eviction order should be granted.

The judgment is a reminder that legal disputes are not won on the facts alone. Even where a landlord has a legitimate grievance, a defective notice can bring an eviction application to a halt before a court ever considers the merits of the case.

The lesson extends beyond landlord-tenant disputes. Small drafting errors in legal notices can have significant consequences, particularly where rights and obligations depend on clear communication.

A properly drafted notice can prevent costly litigation. If you are considering cancelling a lease or pursuing an eviction, obtaining legal advice before taking formal steps may help avoid costly delays and unnecessary disputes.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact us for specific and detailed advice.

© LawDotNews

May 2026 | Property

“The buyer needs a hundred eyes, the seller not one.” (George Herbert)

A Marina Da Gama property. A collapsed wooden deck. A purchase price of R1.55 million and repair costs claimed of just over R100 000. The facts are not complicated. But the legal battle that followed lasted more than a decade.

What happened

The buyers purchased a residential property in October 2013 after the estate agent described it as being in stunning condition. They took occupation in January 2014. Seven months later, the upper wooden deck collapsed. Expert evidence subsequently confirmed that the decks had been constructed without approved plans and were not built to National Building Regulations standards. The defects were latent, meaning they were not visible to a layperson on inspection.

The buyers pursued the estate agent, his close corporation, and the seller across eight separate claims. At the close of the buyers’ case, the defendants asked the court to dismiss the matter on the basis that insufficient evidence had been presented against them. The court agreed and dismissed all the claims.

“Stunning” is not a structural warranty

The buyers argued that the estate agent’s description of the property as being in “stunning” or “beautiful” condition amounted to an actionable misrepresentation. The court disagreed.

Descriptive sales language of that kind is puffery. It reflects aesthetic opinion, not structural fact. It does not amount to a representation about the integrity of the building, compliance with approved plans, or the absence of latent defects. To cross from puffery into misrepresentation, a statement must assert a verifiable fact. Words like “stunning” do not do that.

The estate agent’s duty of disclosure, under the legislation applicable at the time, extended to material facts within his personal knowledge. It did not require him to conduct engineering or technical investigations to uncover hidden structural defects. The defects would not have been visible to a layperson. They were not within his knowledge. No actionable misrepresentation was established.

The voetstoots clause held

The sale agreement contained a voetstoots (as it stands) clause. To defeat it, the buyers were required to prove two things: that the seller had actual knowledge of the latent defect, and that he deliberately concealed it with the intention to defraud.

Neither was established. The buyers’ own evidence undermined the claim. Both buyers described the seller as a decent, honest person. One stated plainly that the seller did not know about the defects. Quick-fix repairs noted by the experts did not change that conclusion. Repairs may reflect ordinary maintenance. They do not, on their own, establish knowledge of a structural defect or an intention to deceive. Fraud is not lightly inferred.

Getting the damages calculation wrong

Even if the buyers had established liability, their damages claim faced a separate problem. The actio quanti minoris, a claim for a reduction in the purchase price, entitles a buyer to compensation for the property’s reduced value caused by the defect. The reasonable cost to repair may serve as evidence of that reduction, but no more. The buyers simply claimed replacement costs, which was entirely the wrong way of going about it.

In plain terms

Puffery is not a promise – in fact, it’s to be expected in real estate listings. A voetstoots clause is not easily defeated. And the burden of investigating a property before signing rests firmly on the buyer.

Nine court days. Twelve years. Presumably substantial legal costs. Every claim dismissed. Get advice before you sign, not after the deck collapses.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact us for specific and detailed advice.

© LawDotNews

May 2026 | Property, Tax, Wills and Estate Planning

“I can’t afford to die; I’d lose too much money.” (George Burns, comedian)

At the heart of any estate plan lies your will. Pair it with a file containing all the information and documents that your executor and heirs will need to wind up your estate, and you’ve laid a solid foundation for protecting your loved ones when you’re no longer around to do so.

Hopefully, most of us have already crossed those two essentials off our “to do” list. But there’s a third step which doesn’t always receive the attention it requires: planning for the costs your estate will have to pay, including a number of taxes.

As with all things to do with SARS and tax, there are many detailed requirements and grey areas involved, so what follows is a general guide only. It’s no substitute for specific professional advice.

The big costs you should plan for

- Costs: Central to your estate planning will be understanding just how much each of your heirs will actually receive from your estate after costs, the most significant of which are usually executor’s fees and government taxes.

- Taxes: There are two main taxes to consider: estate duty, and capital gains tax (CGT). In this article, we’ll focus on the CGT aspect for the simple reason that it’s often forgotten about, and even more often misunderstood.

CGT: The ambush tax lurking in the wings

CGT is one of those low-profile taxes that lurks around unobtrusively in the wings, being ignored and forgotten about until it suddenly pops out of the woodwork.

In this case, the “popping out of the woodwork” will happen when you’re no longer around to be ambushed by it. That’s because CGT is triggered by a taxpayer’s death, which is a “deemed disposal” tax event. In other words, your assets are deemed to have been sold at market value on the day you died. And that triggers a tax liability for your estate on the asset’s growth in value since you acquired it – the capital gain.

Before we get into the nitty-gritty of putting figures to that liability, let’s share a smidgen of good news.

The good news: 3 big exclusions, boosted by Budget 2026

Note firstly that no CGT at all is payable on “personal-use assets”, retirement fund benefits and most mainstream life policies.

Secondly, there’s “spousal rollover relief”: liability for CGT on assets left to your spouse is “rolled over” so that it’s payable not by your estate but later on by your spouse (on sale) or by their estate (on death). That, of course, can make a tremendous practical difference in ensuring that your spouse will be okay financially.

Thirdly, the annual exclusion in year of death, the primary residence exclusion and the small business disposal exclusion can all reduce CGT substantially. And as we note below, Budget 2026 has boosted them all. Good news indeed!

- Annual exclusion in year of death: If you sell assets during your lifetime, your CGT liability is reduced by an annual exclusion of R50,000 (up from R40,000). In the year of your death, this exclusion is boosted to R440,000 (previously R300,000).

- The primary residence exclusion: This is a big one for property owners in respect of their “primary residence” (the home you ordinarily live in), with the exclusion increased from R2,000,000 to R3,000,000.

- The small business asset disposal exclusion: If you leave a small business with a market value of up to R15,000,000 (previously R10,000,000), your estate may qualify for a R2,700,000 exclusion (was R1,800,000) on the assets of the business, which are deemed to have been disposed of on your death. Many small businesses will also qualify for wear-and-tear on assets used in the business. Quantifying this requires professional assistance.

How to calculate CGT

Now for the actual CGT calculation, which will give you a rough idea of the final liability so you can plan for it:

- Include all your assets (except those mentioned above as not being subject to CGT) at their current market value.

- Deduct the base cost of each asset; that is what you bought the asset for plus allowable costs such as costs of acquisition and the cost of subsequent capital improvements.

- Calculate the capital gain or loss by subtracting the base cost from the market value.

- Deduct all exclusions from the capital gain to calculate the net gain.

- Multiply the net gain by the 40% inclusion rate to give you the taxable capital gain.

- Finally, apply your marginal tax rate to that taxable capital gain to give you the final CGT liability.

Putting together a comprehensive estate plan, anchored by your will, is essential to ensure that your loved ones are properly catered for after you’re gone. You know who to call if you need any help!

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact us for specific and detailed advice.

© LawDotNews

May 2026 | Property

“A creature with a big enough head to make a contract should have the sense to make one it can keep.” (Barbara Kingsolver)

A R1.725 million deposit. A bank guarantee that never arrived. A property that ultimately sold for significantly less than the original price. What happens to the deposit money?

A sale that fell apart

The seller agreed to sell an agricultural property in Kyalami for R17.25 million. The purchaser paid a deposit of R1.725 million into the estate agent’s trust account. The balance of the purchase price was to be secured by a bank guarantee on request.

The seller called for the guarantee and gave 14 days to comply. When it was not provided, a further notice gave five business days to remedy the breach. The guarantee was still not furnished. The seller cancelled the agreement and claimed the full deposit.

The purchaser attempted to recover it, but the claim failed.

Rouwkoop or penalty clause?

A true rouwkoop clause – from the Dutch for “regret-purchase” – allows a party to withdraw from a sale by paying a fixed amount. It is an agreed exit mechanism, not a consequence of breach. A forfeiture clause operates differently. It is triggered by breach and is subject to the Conventional Penalties Act. The clause in this case fell into the latter category. The purchaser’s only remaining recourse was section 3 of the Act, which allows a court to reduce a penalty if it is out of proportion to the prejudice suffered.

Why the deadline mattered

The purchaser argued that the word “timeously” meant within a reasonable time, not strictly within the five-day notice period. The court rejected that argument.

Read in context, the agreement created a clear notice-and-remedy mechanism. The five-day period was the operative timeframe. “Timeously” did not introduce flexibility. It referred back to the period expressly stipulated in the contract.

Once the guarantee was not provided within that period, the seller’s right to cancel arose. What the purchaser might have done after the deadline was irrelevant.

Can the court step in?

The purchaser invoked section 3 of the Conventional Penalties Act. That argument did not succeed.

The court looked beyond the arithmetic. It considered the broader consequences of the failed transaction, including the collapse of an onward purchase, the loss of a prior offer, bridging finance, and extended holding costs.

On that evidence, the seller’s prejudice was substantial. The forfeited deposit bore a reasonable relationship to that prejudice. There was no basis for interference.

The real lesson

Deadlines in property transactions are not flexible unless the agreement says so. A deposit is not a placeholder and sellers don’t have to play nice. The bottom line? Get advice before you sign.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact us for specific and detailed advice.

© LawDotNews

April 2026 | Property

“Good rules make good neighbours.” (Old proverb, updated)

The many benefits of living in a residential complex come, naturally enough, with obligations as well as rights.

With its innate potential for conflict between competing rights, community living requires a fine balancing act between the individual rights of owners and residents, and the rights of the community as a whole.

Good rules make good neighbours

Which is of course where a complex’s rules and regulations come into play. Rules provide a structured framework to regulate issues of common concern. Management rules concentrate on administrative and financial issues, while conduct rules (which we’ll focus on in this article) address issues such as noise, pets, parking, use of common property and so on. They are essential not only for protecting everyone’s individual and communal rights, but also to minimise disputes, ensure long-term sustainability and maintain property values.

A well-managed complex benefits everyone – residents, investors, landlords etc.

The sight-impaired owner and his washing machine

Of course, conduct rules are meaningless without enforcement, and that exposes everyone concerned to another balancing act: consistent enforcement versus over-rigid and unconstitutional enforcement.

A recent Supreme Court of Appeal (SCA) decision highlighted this in the case of a complex with a communal washing area.

Before buying his unit in a complex in Gauteng, a visually-impaired man was assured by the estate agent – incorrectly as it turned out – that he would be entitled to modify the washing area directly outside his unit. He duly, without body corporate authority, moved his washing machine into the area and installed piping and a tap, with a security gate and plastic roof sheeting to protect it from the elements. All this, he said, was necessary both to ensure his safety (he cited the danger of slipping in water leaks which he wouldn’t be able to see) and security for his washing machine and clothes.

The body corporate was having none of that and removed the gate and plastic sheeting, citing its conduct rules which prohibit any owner from making alterations to the common washing area. It refused his request for an exemption from the rules on account of his visual impairment, a mediation attempt failed, and eventually his appeal against a CSOS (Community Schemes Ombud Service) ruling found its way to the SCA.

What came out in the wash

The end result? The body corporate is ordered to allow the owner exclusive use of a portion of the common washing area for his washing machine, plus he can install a protective cover over it at his own expense. He must maintain both in good repair, cannot damage the common area wall, has to pay a contribution levy, and must make good all changes when he leaves.

The Court’s reasoning gives us a clear roadmap to our rights, both as bodies corporate and HOAs trying to enforce rules and regulations, and as owners feeling prejudiced by unjustifiably rigid enforcement of them:

- The duty to reasonably accommodate persons with disabilities: Our Constitution prohibits unfair discrimination and enshrines a right to dignity and equality as per the Promotion of Equality and Prevention of Unfair Discrimination Act (PEPUDA) which prohibits any failure to take steps to reasonably accommodate persons with disabilities.

- When rigid enforcement of rules isn’t justified: The body corporate’s refusal to accommodate the owner in this case didn’t take into account that his modifications were necessary for safety reasons, they were proportionate, tailored for his disability, and confined to what he considered essential to prevent harm to himself. They caused no undue inconvenience or hardship to other members of the scheme, nor any expense for the body corporate. Its rigid attitude in enforcing its conduct rules was not justified, and its failure to give him its conduct rules electronically or in Braille was unjust.

- What does “reasonable accommodation” entail? Perhaps the most critical of the Court’s findings is this: “To achieve the objective of equality, I find that reasonable accommodation in a case like this may include allowing structural modifications, granting exclusive rights or exempting disabled residents from burdensome rules.”

- The “minimum hardship to members” principle: At the same time, a body corporate must, in establishing what is and isn’t reasonable in the circumstances, “espouse the principle of minimum hardship to its members”. Witness the strict limits imposed by the Court in this case on the unit owner’s rights of usage.

Thin end of the wedge or just a balancing act?

There may be some concern amongst bodies corporate and HOAs that this is the “thin end of the wedge” when it comes to effective enforcement of rules and regulations. When faced with individual requests which go against the rules and regulations, where should bodies corporate and HOAs draw the line?

Ultimately, the safest course is probably to keep on performing that delicate balancing act we mentioned above, plotting a careful course between individual and communal rights fairly, impartially and reasonably. Common sense isn’t as common as it should be.

Whether you’re an owner, body corporate or HOA, we’re here to help you plot that course!

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact us for specific and detailed advice.

© LawDotNews

March 2026 | Property

“It is a comfortable feeling to know that you stand on your own ground. Land is about the only thing that can’t fly away.” (English novelist Anthony Trollope)

With interest and home loan rates at their lowest since 2022, it’s no surprise that South Africa’s property market confidence level at the end of 2025 was sitting at a record high of 87%. That will have been boosted by the country’s positive economic outlook following Budget 2026, and by Budget 2026’s 50% increase in the primary residence exclusion (which should stimulate sales by reducing the CGT payable by sellers).

If you are a buyer about to put in an offer on a house, remember to budget for the various costs you’ll face over and above the purchase price. In all the excitement of your purchase (particularly if it’s your first house!) it’s easy to underbudget. But you really don’t want to risk any unpleasant financial surprises. If you do breach a term of the sale agreement by not paying something on time, you could even face cancellation of the sale and a damages claim.

Only with a proper budget and cash flow forecast can you be confident both that you really can afford to offer for the house you’ve fallen in love with, and that you’ll be able to pay everything you need to, when you need to.

Have a look at the list we’ve put together below and use it to prepare your own detailed cash flow forecast. Ignore anything that doesn’t apply to you and bear in mind that every buyer’s situation will be unique, so this is no more than a generalised checklist.

Costs payable before transfer

- The deposit: Most sale agreements – often titled as an “Offer to Purchase” (OTP) until it’s accepted by the seller – require you to pay a deposit, usually 5% or 10% of the purchase price.

- Bond/home loan initiation fee: This fee normally incorporates a valuation fee and is added to your loan, but check with whichever bank you use.

- Homeowner’s insurance policy and life cover policy (if required by the bank): Be sure to provide for payment of the first premiums before bond registration.

- Balance of the purchase price: If the deposit you paid and the bond you took out don’t cover the full price, you’ll need to pay the balance before transfer.

- Transfer duty: Unless VAT applies to the sale, transfer duty is payable. This is a government tax payable via SARS before transfer. It applies to all property sales over R1,210,000, on a sliding scale linked to the sale price. This can be a substantial cost!

- Transfer fees: The transferring attorney (conveyancer) charges fees based on a sliding scale linked to the sale price. Added to the account will be charges for FICA verification, deeds searches, postages and petties, other disbursements and the like.

- Bond registration fees: If you take out a bond, the bank appoints an attorney to register it, with the fees calculated on the size of the loan and including the attorney’s fees, FICA charges and a prescribed Deeds Office registration fee.

- Deeds Office fees: These are government charges for both transfer and bond registration.

- Rates clearance: Your local municipality will require advance pro-rata payment of municipal rates before it issues the necessary clearance certificate.

- Levy clearance: Similarly, if you are buying into a complex, the sectional title’s body corporate or Homeowners’ Association (HOA) will require pro-rata levy payments before issuing a clearance certificate.

- Occupational interest (if applicable): If you take occupation before transfer, you need to budget for whatever occupational interest is provided for in the sale agreement.

- Utility deposits: If required by your local municipality when opening up water and electricity accounts.

- Moving costs: Don’t overlook these when budgeting!

Some of these costs are easily overlooked, but they can add up alarmingly. So, plan for them all before you put in your offer to purchase.

Ongoing monthly costs after transfer

Include bond instalments, municipal rates and taxes, levy payments (if you buy in a sectional title or HOA), utility charges, insurance premiums for the property and the contents, and so on.

One-off costs after transfer

If you plan to do alterations or repairs, redecoration, garden revamps, furniture replacement or anything similar, add these costs to your budgeting so you don’t suddenly run out of money and have to postpone them. For long-term planning, set aside a budget for ongoing home maintenance.

As always, we are here to assist, so let us know if you have any questions, need any further information, or would like help in creating a cash-flow projection specific to your purchase.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact us for specific and detailed advice.

© LawDotNews