“Things do not go away. They go somewhere.” (Annie Dillard)

Many trustees assume that a dormant trust can be safely forgotten. No income, no assets, no transactions … No problem.

SARS has made it clear that this assumption may be an expensive one.

In recent months, SARS has intensified its focus on trust compliance, targeting trusts that have failed to submit annual income tax returns. What many trustees may not realise is that inactivity does not remove a trust’s tax obligations.

A trust that has been sitting dormant for years is still required to submit annual income tax returns. Failure to do so can now result in administrative penalties, even where the trust has conducted little or no activity.

Dormant does not mean exempt

One of the most common misconceptions among trustees is that a trust only has compliance obligations if it earns income, owns assets, or actively conducts transactions.

That is not how SARS views the issue.

According to SARS, all registered trusts, whether economically active or passive, are required to submit annual income tax returns. The obligation exists even where the trust has little or no economic activity.

Why SARS is paying closer attention

Since May 2026, the revenue authority has been issuing administrative penalty assessments to trusts with outstanding returns following earlier final demands for compliance. Trustees who received those demands were given an opportunity to correct the non-compliance before penalties were imposed.

Depending on a trust’s assessed taxable income, monthly administrative penalties can range from R250 to R16,000 and may continue accruing if the non-compliance is not remedied.

This reflects a broader shift in SARS’ approach to trusts. What was once viewed by many as a relatively passive area of administration is increasingly becoming an area of active oversight and enforcement.

Thinking about winding up a trust?

Many trustees only discover outstanding compliance issues when they begin taking steps to terminate a trust’s affairs. By that stage, years of outstanding returns, incomplete records, or unresolved SARS obligations may need to be addressed before the process can move forward.

Importantly, a trust that has effectively ceased operating is not automatically regarded by SARS as deregistered for tax. Trustees remain responsible for ensuring that trust information is maintained, updated, and, where appropriate, formally deregistered through the correct processes. Failure to do so may expose the trust, and potentially its trustees in their capacity as representative taxpayers, to penalties and other consequences under the Tax Administration Act.

Winding up a trust and deregistering it with SARS are not the same thing. A trust that trustees regard as dormant, inactive, or terminated is still regarded by SARS as a registered taxpayer with ongoing filing obligations until it has been properly deregistered.

The position can become particularly costly where penalties have been accumulating in the background.

As SARS continues to invest in data capabilities and automated enforcement mechanisms, historic compliance issues are becoming easier to identify and harder to overlook. In some cases, trusts that trustees believed were inactive for years are now being drawn back into the compliance net.

The lesson is straightforward: before assuming that a dormant trust requires no further attention, trustees should ensure that all filing obligations have been met and that the trust’s SARS records are up to date. A trust may be dormant in practice, but that does not mean it has disappeared from SARS’ radar.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact us for specific and detailed advice.

“I can’t afford to die; I’d lose too much money.” (George Burns, comedian)

At the heart of any estate plan lies your will. Pair it with a file containing all the information and documents that your executor and heirs will need to wind up your estate, and you’ve laid a solid foundation for protecting your loved ones when you’re no longer around to do so.

Hopefully, most of us have already crossed those two essentials off our “to do” list. But there’s a third step which doesn’t always receive the attention it requires: planning for the costs your estate will have to pay, including a number of taxes.

As with all things to do with SARS and tax, there are many detailed requirements and grey areas involved, so what follows is a general guide only. It’s no substitute for specific professional advice.

The big costs you should plan for

Costs: Central to your estate planning will be understanding just how much each of your heirs will actually receive from your estate after costs, the most significant of which are usually executor’s fees and government taxes.

Taxes: There are two main taxes to consider: estate duty, and capital gains tax (CGT). In this article, we’ll focus on the CGT aspect for the simple reason that it’s often forgotten about, and even more often misunderstood.

CGT: The ambush tax lurking in the wings

CGT is one of those low-profile taxes that lurks around unobtrusively in the wings, being ignored and forgotten about until it suddenly pops out of the woodwork.

In this case, the “popping out of the woodwork” will happen when you’re no longer around to be ambushed by it. That’s because CGT is triggered by a taxpayer’s death, which is a “deemed disposal” tax event. In other words, your assets are deemed to have been sold at market value on the day you died. And that triggers a tax liability for your estate on the asset’s growth in value since you acquired it – the capital gain.

Before we get into the nitty-gritty of putting figures to that liability, let’s share a smidgen of good news.

The good news: 3 big exclusions, boosted by Budget 2026

Note firstly that no CGT at all is payable on “personal-use assets”, retirement fund benefits and most mainstream life policies.

Secondly, there’s “spousal rollover relief”: liability for CGT on assets left to your spouse is “rolled over” so that it’s payable not by your estate but later on by your spouse (on sale) or by their estate (on death). That, of course, can make a tremendous practical difference in ensuring that your spouse will be okay financially.

Thirdly, the annual exclusion in year of death, the primary residence exclusion and the small business disposal exclusion can all reduce CGT substantially. And as we note below, Budget 2026 has boosted them all. Good news indeed!

Annual exclusion in year of death: If you sell assets during your lifetime, your CGT liability is reduced by an annual exclusion of R50,000 (up from R40,000). In the year of your death, this exclusion is boosted to R440,000 (previously R300,000).

The primary residence exclusion: This is a big one for property owners in respect of their “primary residence” (the home you ordinarily live in), with the exclusion increased from R2,000,000 to R3,000,000.

The small business asset disposal exclusion: If you leave a small business with a market value of up to R15,000,000 (previously R10,000,000), your estate may qualify for a R2,700,000 exclusion (was R1,800,000) on the assets of the business, which are deemed to have been disposed of on your death. Many small businesses will also qualify for wear-and-tear on assets used in the business. Quantifying this requires professional assistance.

How to calculate CGT

Now for the actual CGT calculation, which will give you a rough idea of the final liability so you can plan for it:

Include all your assets (except those mentioned above as not being subject to CGT) at their current market value.

Deduct the base cost of each asset; that is what you bought the asset for plus allowable costs such as costs of acquisition and the cost of subsequent capital improvements.

Calculate the capital gain or loss by subtracting the base cost from the market value.

Deduct all exclusions from the capital gain to calculate the net gain.

Multiply the net gain by the 40% inclusion rate to give you the taxable capital gain.

Finally, apply your marginal tax rate to that taxable capital gain to give you the final CGT liability.

Putting together a comprehensive estate plan, anchored by your will, is essential to ensure that your loved ones are properly catered for after you’re gone. You know who to call if you need any help!

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact us for specific and detailed advice.

“We are also proposing additional tax measures to ease the financial burden on households and businesses, by adjusting personal income tax brackets and rebates fully in line with inflation.” (Minister of Finance Enoch Godongwana)

How much will I save if I sell my house?

A big highlight for property sellers and buyers is that, having remained unchanged since 2012, the primary residence exclusion for Capital Gains Tax has been increased from R2 million to R3 million. In addition, the annual CGT exclusion has been increased for individuals by 25% from R40,000 to R50,000, and for deceased estates by 47% from R300,000 to R440,000.

The big win is that when you sell your primary residence (the home you live in), the first R3 million capital gain is now excluded from CGT.

Have a look at the illustrative savings calculation below:

Primary residence CGT exclusion: R2m vs R3m

Transfer duty threshold unchanged

Unchanged from last year, you pay no transfer duty if the property you are buying sells for at (or below) the set threshold of R1,210,000.

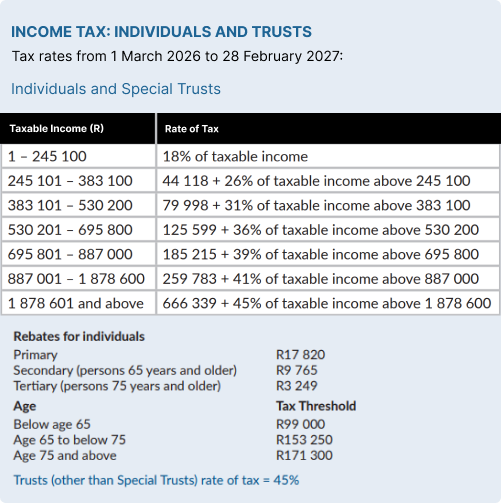

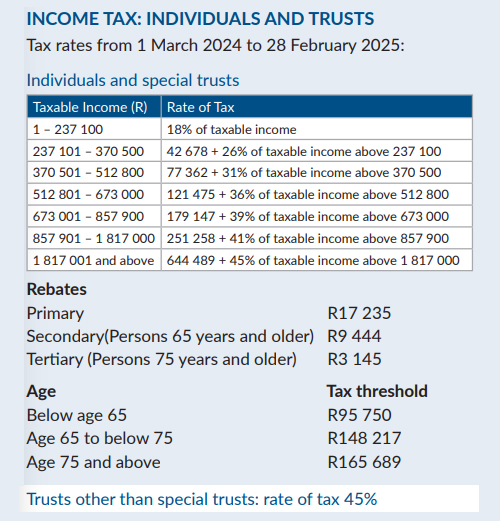

Individual taxpayers:Your tax rates (and the associated rebates and medical tax credits) are increased in line with inflation. That’s welcome relief after last year’s unchanged tax tables which resulted in “fiscal drag” (also referred to as “bracket creep”) for anyone receiving a salary increase that pushed them into a higher tax bracket.

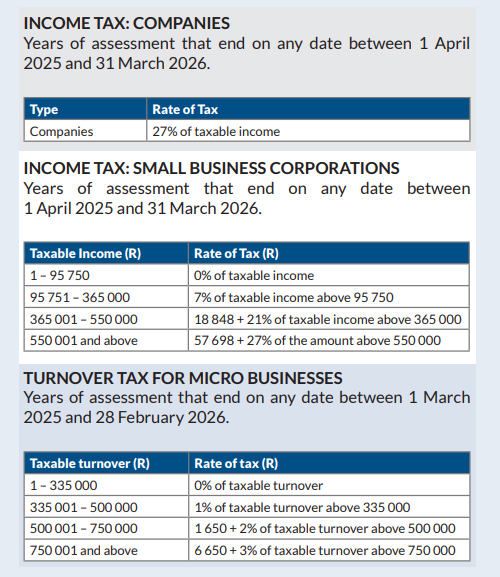

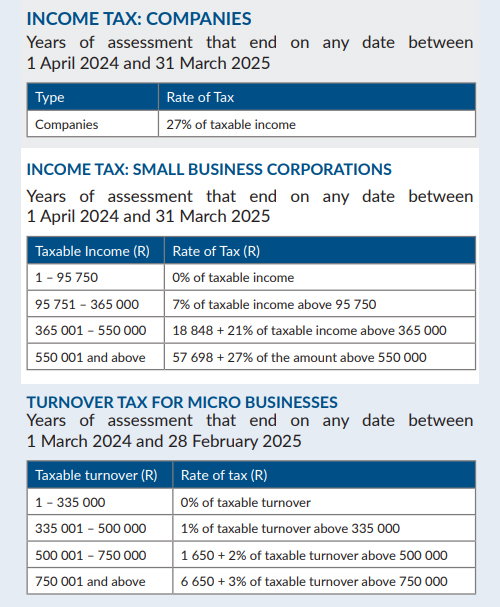

Trusts: Special trusts are by and large taxed as individuals, but other trusts are taxed at a flat rate of 45% – also unchanged from last year.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact us for specific and detailed advice.

You pay no transfer duty if the property you are buying sells for less than the set threshold. The threshold wasn’t increased last year, so this year’s proposed 10% increase from R1,100,000 to R1,210,000 (from 1 April) is a welcome adjustment for inflation.

With all the brackets adjusted upwards by 10% as per the table below, properties at every level become that much more affordable to buyers, and by extension sellers will also benefit.

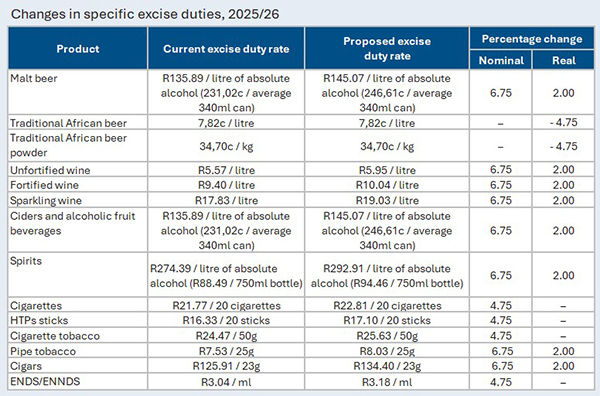

The proposal to increase VAT from 15% to 16% over two years, with a 0.5% hike planned to take effect on 1 May 2025 and the other 0.5% on 1 April 2026, has met with fierce resistance from business, consumers and trade unions – and from the opposition benches in parliament.

As to when we can expect clarity on whether government will be able to muster enough support in parliament to convert this and its other proposals into law, we are sailing in uncharted waters and only time will tell. Hold thumbs!

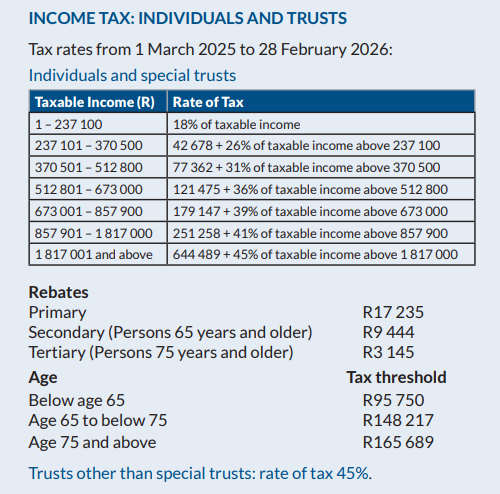

The unchanged tax tables, and no new taxes

Individual taxpayers: Your tax rates (and the associated rebates and medical tax credits) are unchanged, so we can at least be thankful that there were none of the major increases that had been hinted at.

What will hurt us is that for the second consecutive year there is no inflation adjustment to the tax brackets, which means that “fiscal drag” (also referred to as “bracket creep”) will leave you paying more tax if you receive an increase – particularly if it pushes you into a higher tax bracket.

Trusts: Special trusts are by and large taxed as individuals, but other trusts are taxed at a flat rate of 45% – again unchanged from last year.

Corporate and other taxes: Corporate and dividend tax rates, capital gains taxes, donations tax and estate duty all remain unchanged. With all the pre-Budget speculation about possible increases in these taxes, perhaps coupled with a new wealth tax and/or new taxes to fund the NHI (National Health Insurance), this is good news.

How much will you be paying in income tax, petrol and sin taxes? Use Fin 24’s four-step Budget Calculator here to find out.

Note: There is (at time of writing) uncertainty as to whether or not the Minister will proceed with his proposed tax changes – even if he fails to garner sufficient political support to ultimately ensure their adoption by parliament. If he does proceed, it’s equally unclear how long they will be valid for. Regardless, expect a lot of political manoeuvring and perhaps some major changes in the weeks ahead!

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact us for specific and detailed advice.

How much will you be paying in income tax, petrol and sin taxes? Use Fin 24’s four-step Budget Calculator here to find out.

The unchanged transfer duty and tax tables, with a note on fiscal drag

Unchanged from last year, so taxpayers can breathe a sigh of relief that rates have not been increased as many forecasters had feared.

But the other side of the coin of course is that there is no inflation adjustment to the rates this year, which means that “fiscal drag” will leave you paying more tax if your inflation-linked increase pushes you into a higher tax bracket. Effectively, the buying power of your net income will fall. Plus if your property has increased in value into a higher threshold, your buyer will pay more transfer duty.

The proposed “two-pot” retirement reform: Per National Treasury:“Early access to retirement funds – “The two-pot retirement system will allow retirement fund members to make withdrawals from their retirement funds while they are still active members, so members need not resign to access part of their retirement benefits. … This reform is proposed to come into effect on 1 September 2024. The National Treasury aims to finalise the legislative process rapidly in the next few months to ensure that industry and regulators can prepare for implementation. Policy research and engagement continues on the outstanding auto-enrolment, mandatory enrolment and consolidation retirement reforms.”

The proposals and their tax implications are complex and subject to change, but currently provide for a one-off withdrawal of up to R30,000 on implementation, and thereafter annual “savings withdrawal benefits”.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.